Even Before the Iran War, There Was a Growing Inflation Problem

January PCE data reveals that disinflation had already stalled and reversed before the war with Iran. Even before new fiscal stimulus and the energy shock, there's a case for a pause, or even a hike.

Last Friday we got the PCE inflation numbers for January 2026. They showed a growing inflation problem. The genuine progress people could point to by the end of 2024 has slowed or reversed over the second half of 2025. Three months ago I flagged a rough 3-month patch for PCE inflation, and since then it’s gotten worse. This alone, before the war with Iran, would call on the Federal Reserve to pause rate cuts and at least begin gaming out what a rate increase path looks like at their FOMC meeting today.

{kind=link}

I don’t think the severity of this has been conveyed well in the media. Coverage tends to focus on CPI inflation, which is the majority of inputs into PCE, but it is not the Fed’s target and is being pulled lower by its heavier weight on housing. Important methodological debates have taken up airtime. And when PCE is discussed, it’s generally in year-over-year terms, which smooths over how much things have heated up over the past three to six months.1

All of this is before the war with Iran, which started on February 28th. The problem existed before the energy shock that is now ongoing. WTI crude is running roughly $30 above its pre-war level, and the hit to production and consumer spending would on its own put the central bank on pause. As Bob Elliott notes, an oil shock is “like the opposite of a productivity boom.” He finds that historically “the best case scenario is a pause to easing and a worst case scenario is hikes into weakness” in order to maintain expectations.2 The fact that inflation was already a problem before this shock only makes the Fed's position that much harder.

Overall

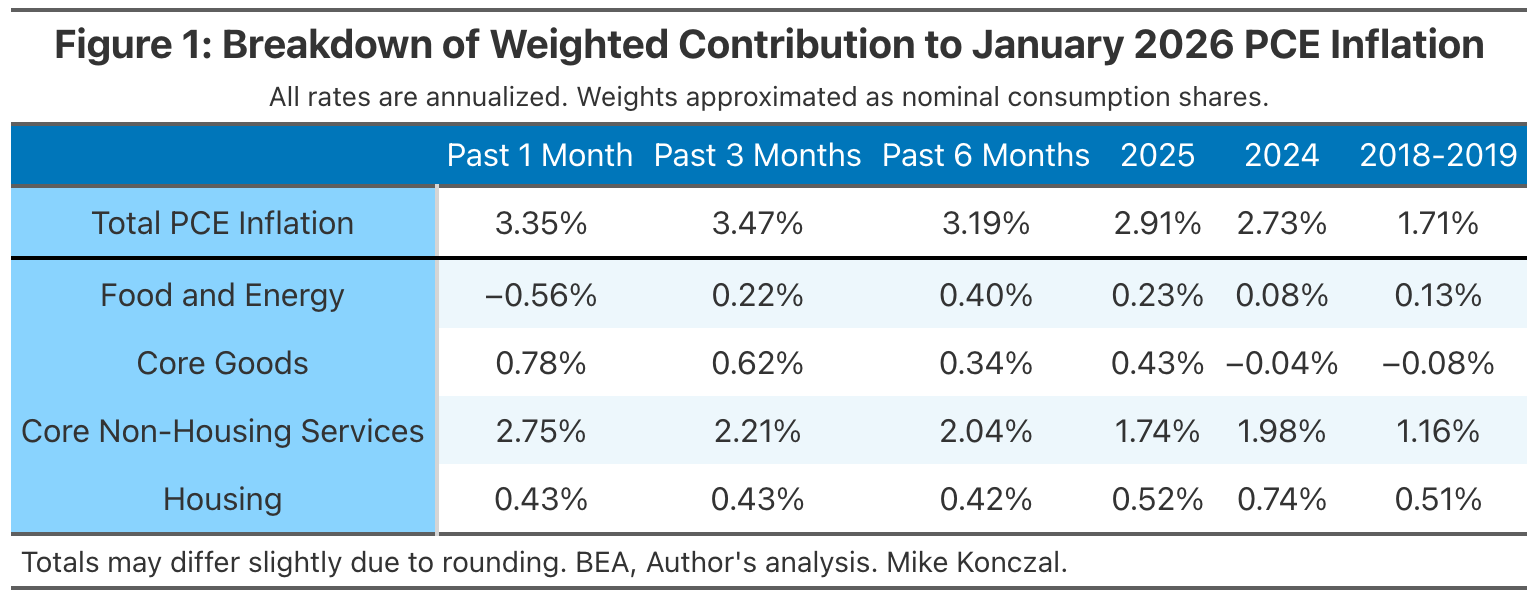

Figure 1 is the chart I follow most closely, the breakdown of PCE inflation by type across several measures. The top line is total PCE inflation over several dates and intervals, and the subsequent lines are how much each part contributes to that total number.

PCE inflation has increased. In 2024, it ran at 2.73%, and there was a clear runway for roughly 0.3 percentage points of decline in housing, which did materialize. That would have gotten inflation closer to target at around 2.4%, with the central bank doing a careful dance through the last mile of disinflation.

Instead, inflation picked up. It ran 2.91% across 2025. Over the past three and six months it ran 3.47% and 3.19%, respectively. It has been accelerating, getting hotter the more recently you look. And that includes banking the housing disinflation that came through on schedule.

What can make this situation better?

Tariffs and Goods

Core goods is a new and significant contributor to inflation, and some of that is tariffs. As a kind of tax on consumption, tariff-driven price increases should be looked through as long as inflation expectations aren’t breaking, and they haven’t. There’s significant debate about how much of the pickup in goods inflation is tariff-driven. The Trump administration is in the awkward position of arguing that core goods inflation is global and structural rather than temporary and driven by their tariff actions, which, if true, means the Fed should probably be tightening.

If we assume half of goods inflation is tariffs, total PCE inflation still sits at or above 3% on the three- and six-month horizon. If we assume all of goods inflation is tariffs, and it would be 0% otherwise, overall inflation is still higher than 2024. We’ve lost ground going into 2026.

We can also just look at non-housing services inflation. This measure was originally emphasized to deal with goods prices spiking on shortages, and here too we see a spike in recent months. It’s contributing a full 2.04 percentage points, the entire target, over the past six months. There’s a problem here.

Market-Based Measures

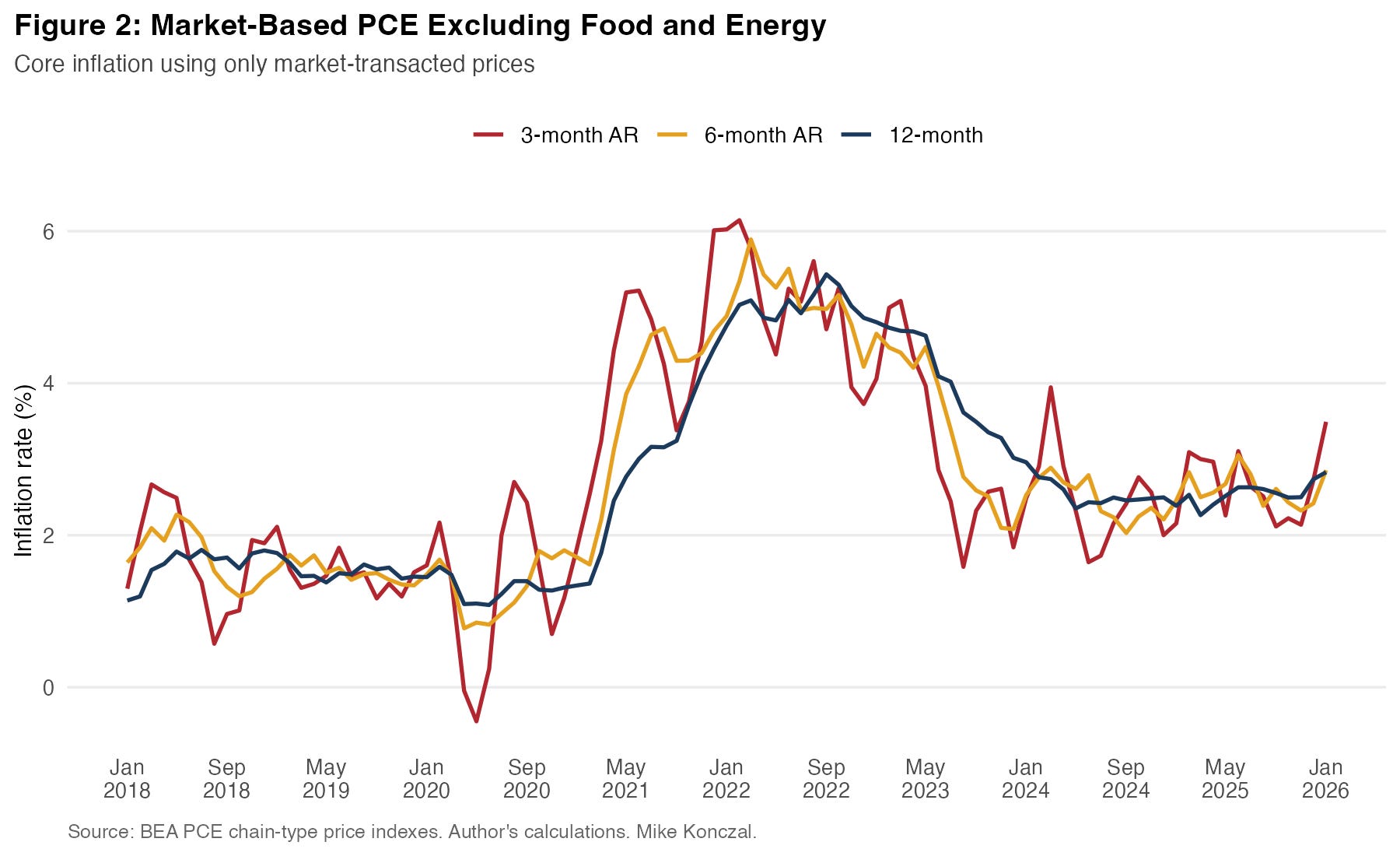

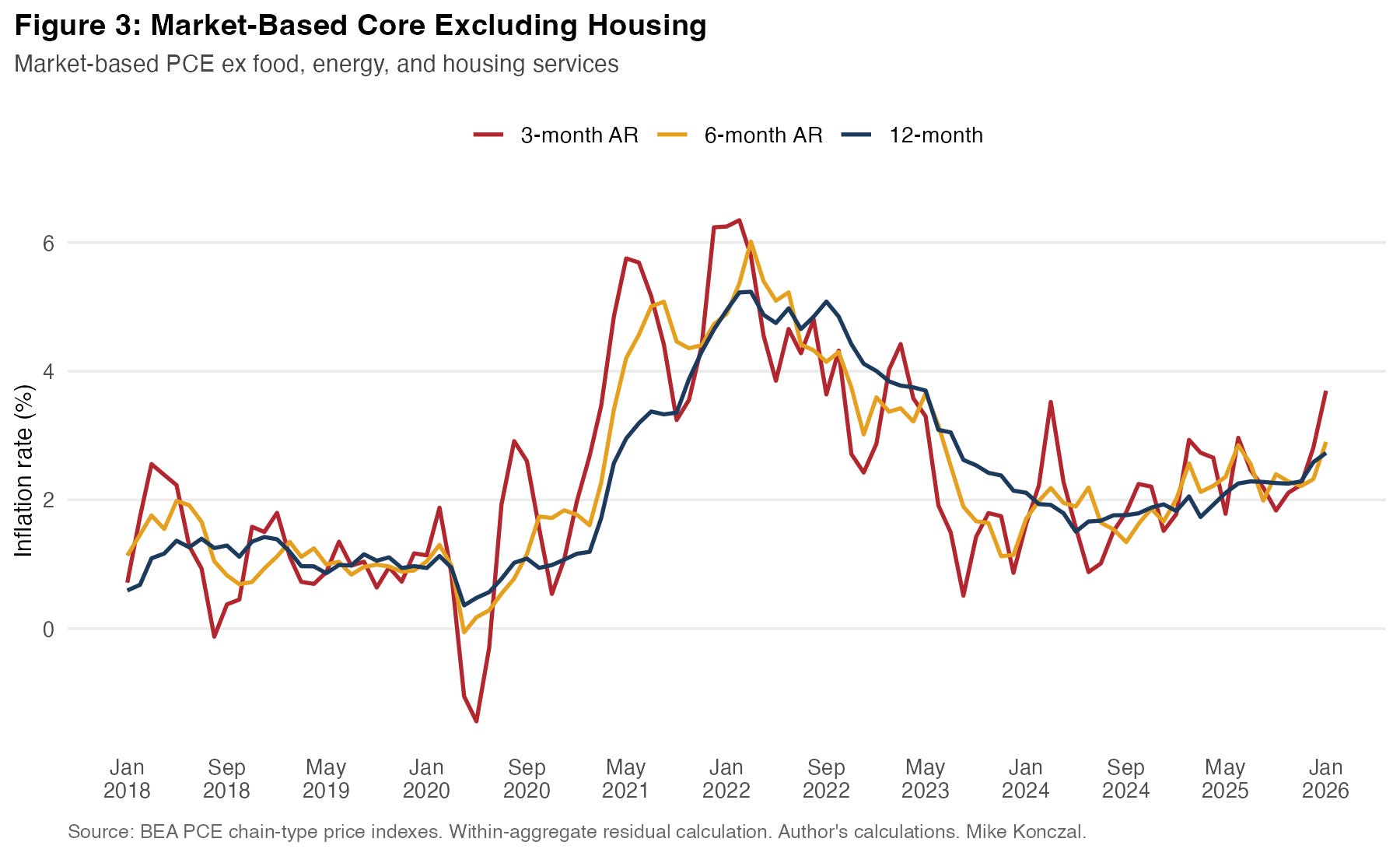

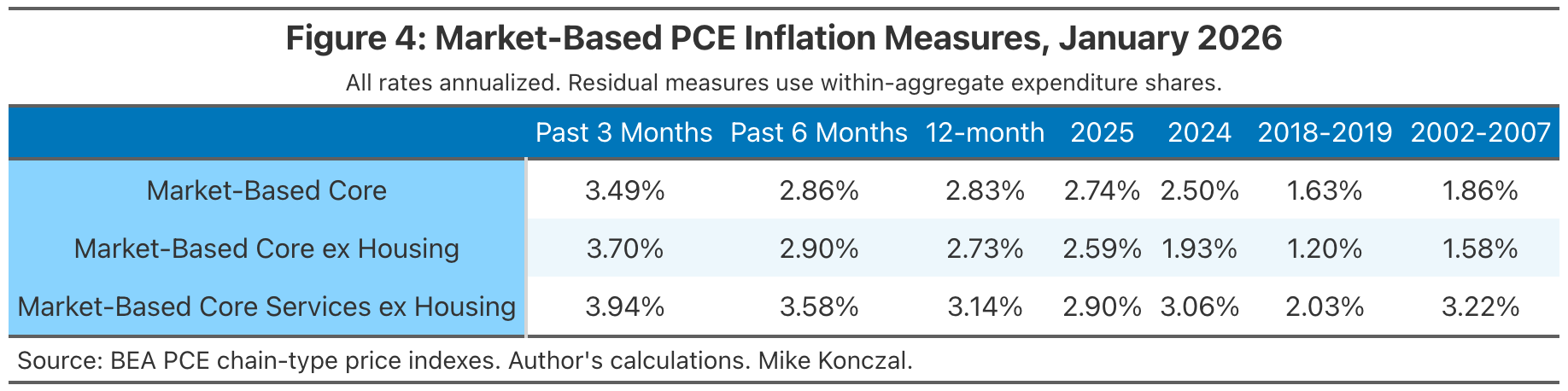

Another move has been to emphasize the imputed elements of core non-housing services, particularly portfolio management services. Stephen Miran of the FOMC emphasized looking at market-based core inflation in a December speech, arguing it showed genuine cooling. Recent months have gone against that analysis.

As Figures 2 and 3 show, market-based core inflation and market-based core excluding housing have accelerated in recent months:

Footnote on creation below.3 Here in Figure 4 are those two series, along with market-based core services ex housing, showing the annualized percent increase in the respective index. So market-based core inflation increased 2.86% over the past six months, compared to 2.5% in 2024.

Every one of these measures has accelerated in recent months. Over the past three, six, or twelve months, they all run higher than their 2024 values (annualized). Miran, in his speech, described 2002-2007 as a period in which overall inflation was at target, and thus a good benchmark for these market-based measures. They are all running much higher than that time period. (Hat-tip to Omair Sharif making this point here.) The various supercore measures, the ones specifically designed to strip out noise and find the underlying signal among imputed prices, are all heating up faster than we’d expect.

Labor Market

Another argument is that the labor market is softening enough to bring inflation down on its own. I think this is more complicated than it looks. The unemployment rate has been essentially flat for almost a year, ranging roughly between 4.3 and 4.4 percent since last May. Average hourly earnings have moved sideways. There is weakness in hiring and openings, and I think young college graduates show a surprisingly high level of unemployment given the headline rate. Personally, I tend to think there are two unemployment numbers, one for those under 26, which has increased, and one for those above, which is more normal.

But the case that the labor market is decelerating fast enough to take pressure off nominal spending growth isn’t there in the data right now.

Fiscal Impulse

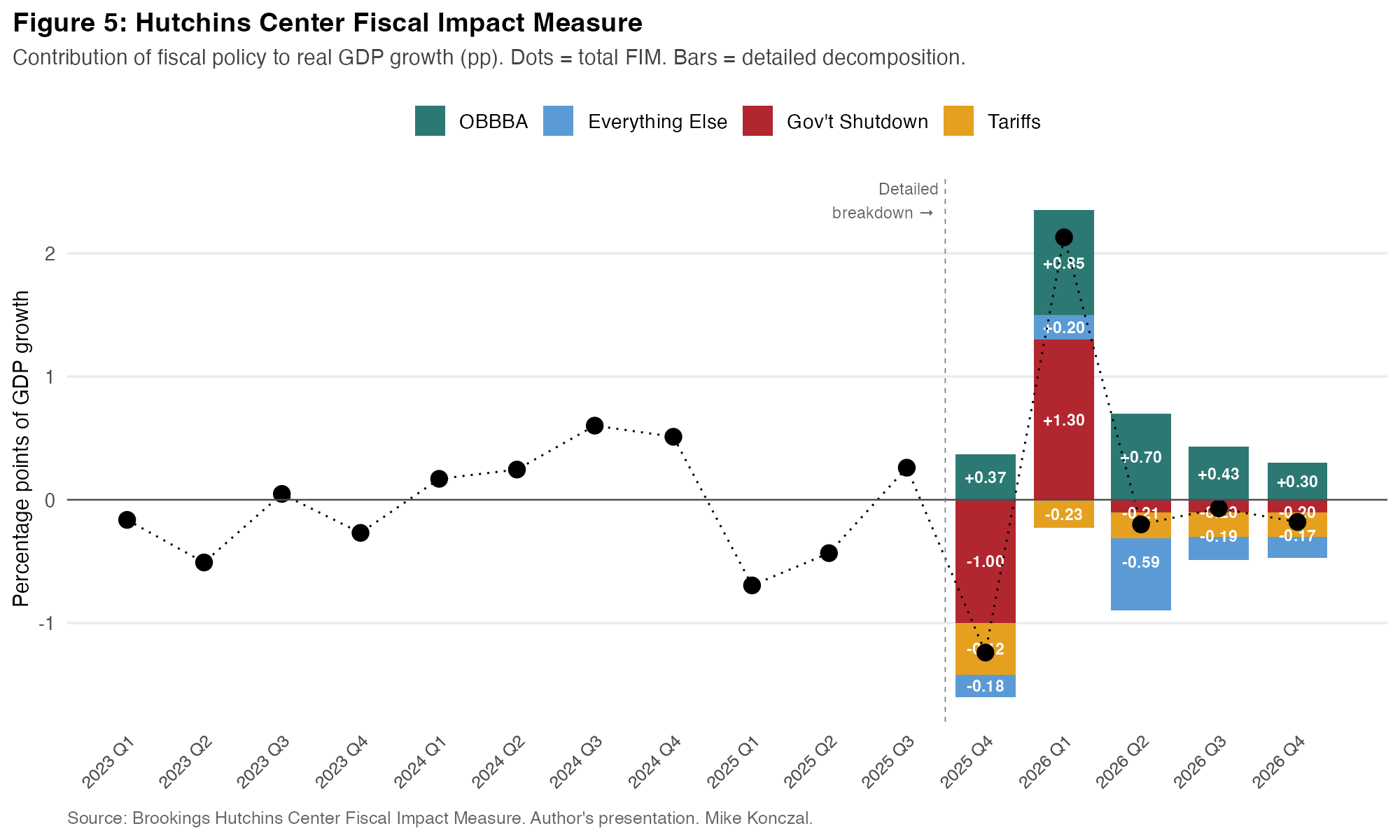

The oil shock is coming. But before that, there was another shock already in the pipeline: the One Big Beautiful Bill Act (OBBBA). Below in Figure 5 is the fiscal impulse tracked by the Brookings Institution Hutchins Center Fiscal Impact Measure, which I’ve followed closely over the years. There’s a government shutdown which is shifting Q4 2025 spending to Q1 2026. But they also note an increase in GDP from “the stimulative effects of the OBBBA on both purchases and taxes.”

Going into the year, the fiscal impulse from OBBBA will be substantial in Q1, and the tariffs do not offset it. Ironically, a massive gas price spike may have arrived just in time to choke off the stimulative effects of OBBBA which was already pouring into a higher-inflation environment. But fiscal impulse is still in play as the Fed looks ahead through 2026, and this is before any additional war spending for Iran, which could get very expensive and become a large additional fiscal impulse if the conflict continues.

How Far Off Is the Fed?

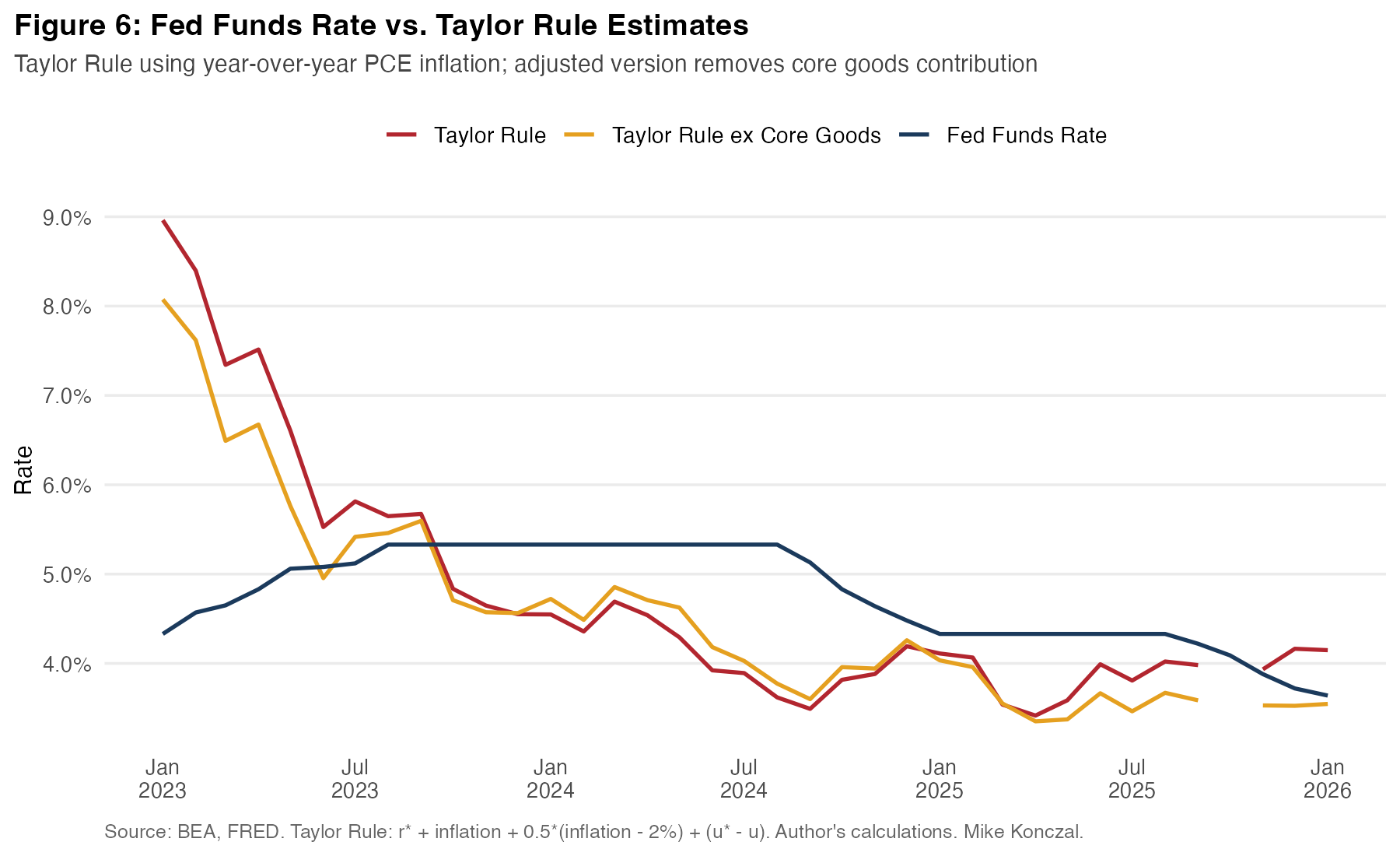

Figure 6 gives us a sense on where the Federal Reserve’s own Taylor Rule would land with a couple of assumptions. Assuming, as the Fed does, that r* is 1% and NAIRU is 4.2%, then the year-over-year value of PCE would have the Fed raising rates. Assuming all core goods inflation would be zero without the tariffs in a year-over-year number has rates basically right where they currently are (yellow line).

This graphic gives a sense of what the Fed was thinking; it understood itself as too tight (the blue Fed funds rate is above measured inflation). However there hasn’t been continued disinflation, and in recent months inflation has picked back up. This graphic reflects year-over-year inflation, which is lower than the inflation rate over the past six or three months, which would have rates from a Taylor Rule even higher. The more the Fed looks at recent information, the more they should be worried they got ahead of things.

There are things the Trump administration could do to try and ease this. Pardon the entire FOMC and back off independence, pick selective tariffs to execute, and stop deportation quotas might be a baseline if they want to wage an ongoing war against Iran. But they seem unlikely to try and prioritize anything, much less their crises putting pressure on aggregate supply while pushing demand.

Maybe this all turns over. Though note that in recent years the second half has been the cooler part of the inflation calendar, even with seasonal adjustments, which makes it running hot especially worrying. The decisions the central bank made made sense as they were happening. But at this point the Fed should not be in any hurry to cut further. That was true even before a major energy war landed on top of everything else.

If you're at the Powell press conference today, all your colleagues are going to have questions about Iran and criminal charges against Powell, so you want something unique. But you likely are stressed hunting down oil and energy sources for stories and having had to watch your kids home from school for the D.C. storm that never came. So steal this blog post for your question! Some questions that'll get attention:

The three- and six-month PCE numbers, both overall and supercore, are running well above target and have been accelerating even before the energy shock.

At what point do shorter-horizon measures like these change the Committee's assessment of where inflation is headed?

How much would this acceleration have to continue in order for the Committee to consider rate hikes?

Looking back, does the Committee believe the December cut was premature given how inflation has evolved since?

Your own Taylor Rule, using the Committee’s r* and NAIRU estimates, suggests rates should be at or above where they are now, whether or not you look through tariffs, and especially above with more recent PCE inflation data. How do you make the case that the current stance isn’t accommodative, especially this far from the inflation target?

Even zeroing out all goods inflation, non-housing services is contributing 2 percentage points on a six-month basis. Is the tariff look-through framework relevant when the non-tariff components are the ones accelerating?

According to estimates, the OBBBA is delivering a meaningful fiscal impulse into an economy where inflation was already reaccelerating. How does the Committee factor that into its outlook?

I have a pet theory the media also covers CPI better because the data release website is much easier to navigate. Want the CPI year-over-year inflation rate for uncooked ground beef and how much it contributed to overall inflation? Check this table. But if you want anything other than headline or core from PCE, good luck navigating that NIPA interface. (I deeply, truly, love the NIPA interface.) Here’s to more realizing you can just download the PCE flatfiles right off that site and automate your work with command-line AI.

Here is how my former boss Lael Brainard described this reasoning when she was on the FOMC, responding to the energy shock that followed Russia's invasion of Ukraine (h/t Matthew Klein):

A protracted series of supply shocks associated with an extended period of high inflation—as with the pandemic and the war—risks pushing the inflation expectations of households and businesses above levels consistent with the central bank’s long-run inflation objective. It is vital for monetary policy to keep inflation expectations anchored, because inflation expectations shape the behavior of households, businesses, and workers and enter directly into the inflation process. In the presence of a protracted series of supply shocks and high inflation, it is important for monetary policy to take a risk-management posture to avoid the risk of inflation expectations drifting above target.

Note market-based core PCE is available via BEA and is accessible on FRED here. The other two are created by me, using percent of nominal expenditures as the weight over the time period. They match other estimates I’ve seen. All the code for graphics and data is here.

What is in "market-based core services ex housing"? Is it mostly healthcare insurance, home insurance, auto insurance, and utilities? Prices of these are set by state regulators, with a long lag. Prices aren't imputed, but they aren't really floating market prices either.