The Weirdness of Jay Powell's Legacy

Plus my favorite video of him, and the tattoo I got in response to the soft landing.

Today is Jay Powell’s last day as Federal Reserve Chair. I think he did a good job. I think he’ll be remembered well.

But let’s start with a video of my favorite Powell moment and then walk through a little bit about why his legacy will be a bit weird in the short term.

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser

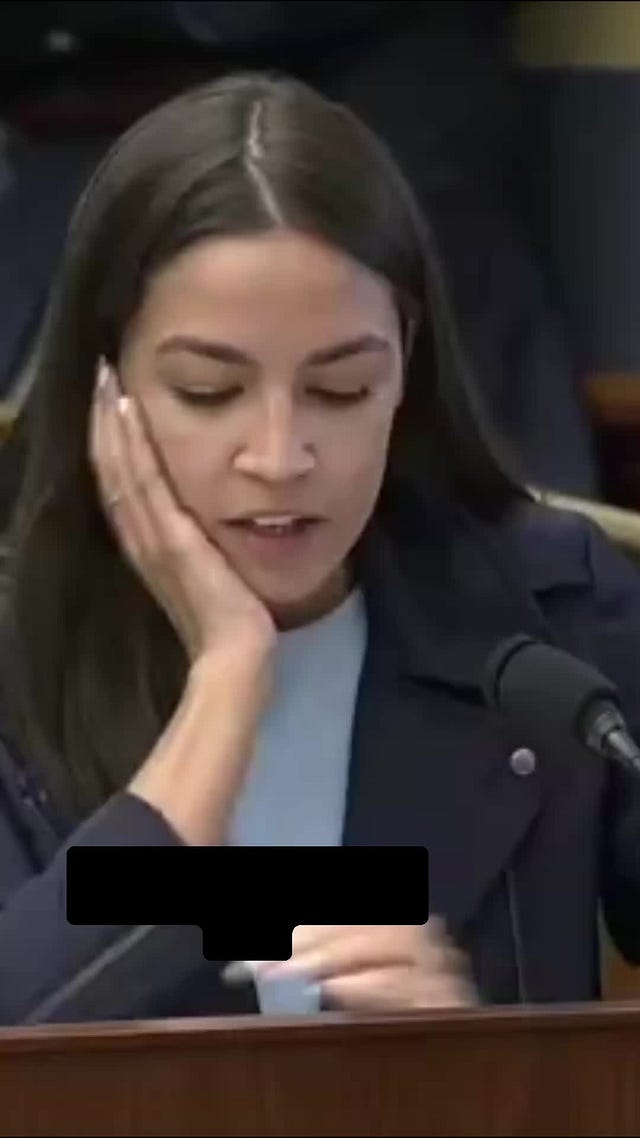

July 10th, 2019, Jay Powell is testifying before the House.

Representative Ocasio-Cortez: In early 2014, the Federal Reserve believed that the long-run unemployment rate was around 5.4%. […] Unemployment has fallen about 3 full points since 2014 [to 3.7%], but inflation is no higher today than it was 5 years ago. Given these facts, do you think it’s possible that the Fed’s estimates of the lowest sustainable unemployment rate may have been too high?

Powell: Absolutely. <laughs>

Having spent some time thinking about this exchange both before and after it happened, I still remain impressed with Powell’s answers and follow-up. (You can see it all on CSPAN here.) It helps that Ocasio-Cortez is a serious politician who took the novel step of asking a relevant and interesting monetary policy question to the Federal Reserve chair. (The Republican representative right before AOC asked Powell whether or not he believes in the market system and whether or not the United States was the greatest economy in history.)

Powell, in his answer and the full clip, demonstrates both command of the material and humility. When AOC follows up on the flattening Phillips Curve, Powell is honest and open about what the Fed knows and what it doesn’t. I think this temperament served him well navigating the great labor market of 2019, the inflation wave that hit, and the soft landing. A more dogmatic and less open Federal Reserve chair would have cut off that 2019 economy (AOC was right that the general consensus was that unemployment couldn’t go below 5%). They also could have forced a recession in 2022-2023 for inflation to come down. But he understood his role was to maintain inflation expectations while staying open to the idea that they could solve it without causing a recession, which they did.

These are admirable qualities in a central banker, and I hope they outlast him.

Now you might read this and watch that clip and say, “Aha, Powell’s dovishness caused the great inflation!” But in the short term, this legacy is weird. People want to hate him for the inflation wave we’ve seen. Defenders point out that the inflation was global and credit him for the soft landing. I just did. But the soft landing was global too.

Let’s grab some quick OECD data. Here’s headline CPI inflation for the United States and several peer countries. This is year over year, over the past several years.

As you can see, it really was global. We could redo this with different measures of inflation or bring in more countries, but, as someone who has sweated these details, it’s all the same thing. It’s hard to either credit or blame Powell for this specifically. In retrospect I’m sure he wished he raised rates earlier, but I have a hard time thinking it would have changed this dynamic, and most realistic estimates (e.g. Reifschneider, 2024) don’t have much of a difference.

But how unique was the soft landing? Let’s also pull unemployment rates and GDP rates from OECD for these countries. Let’s plot the amount of disinflation for each country, from their highest to lowest values, against the annualized cumulative change in the unemployment rate during this period. Not the most sophisticated, but we’ll get the same results if we do the bells and whistles.

The general thought was that you’d need two percentage points of unemployment to bring down inflation one percentage point. This is called the sacrifice ratio with a value of 2, and it is reflected in the solid line above. As a matter of geometry, the soft landing is that you can have high disinflation, a value far to the right, without being near the line. But the actual measured sacrifice ratio is essentially zero. There are many estimates of the sacrifice ratio in the economics literature, generally in the 1-3 range. If the value is near zero, then something else is going on.

Now unemployment is doing a lot of crazy things during this time period, and we’re not trying to adjust it to compare against more normal rates. So let’s look at GDP growth also.

Following Ball (1994) (more methodology details here), we draw a GDP trend line from when inflation peaked to its lowest point and count up the deviations to get the cost to GDP of reducing inflation. As the graphic above shows, that number is also essentially zero. For the United States, it straight up has the wrong sign. The sacrifice ratio is negative.

Here’s a table with all this information.

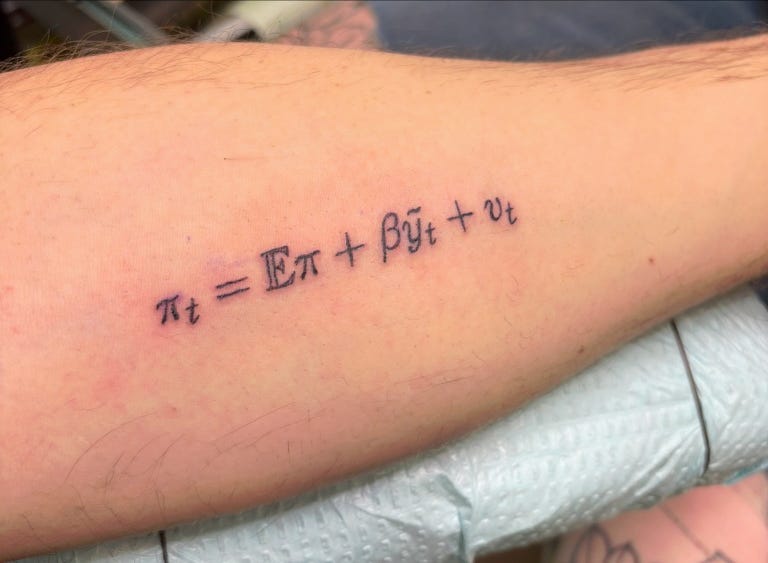

The global soft landing looks easy in retrospect. But to give a sense of the outside chance of this, back when it looked impossible I said I would get a tattoo of the Phillips Curve if we pulled off the soft landing. Which we, and I, did.1

If a variable has the wrong sign, as βy does, then we probably need to look at other variables. And there is one you can see on my left forearm: the cost-push shock v term. If that term did the work, Powell’s job wasn’t engineering a recession to break inflation. It was holding expectations steady while supply healed, and that’s what he did.

If President Trump wanted Powell to be remembered poorly, he single-handedly screwed that up. By putting so much political pressure on him in such a comical yet terrifying way, Trump all but ensured Powell will be remembered quite well for standing his ground. I think, with time, his economic record will be remembered as well too.

I also got this tattoo because my Team Macro Era was truly a wild ride, and as I moved over to different work in the past year it’s something to remember the journey from EconTwitter to the White House, from lots of graphs on data release days to getting to work for the awesome Lael Brainard, and to have a reminder of the general rollercoaster of the last 20 years of macroeconomic instability. Also it’s fun, when people ask what it means, to say “It’s an equation economists use to model inflation. It’s notoriously awful at it.”

I love this, Mike! He was a Fed Chair for the ages, and I'm glad he's sticking around on the Board of Governors.

Banger