Sending in the TANKs Against Citrini's AI Doomerism

In which we use an internet sensation over AI displacement to learn some New Keynesian modeling and the economic possibilities for our grandchildren.

The research firm Citrini recently put out a note titled The 2028 Global Intelligence Crisis. It’s a speculative scenario in which rapid AI-driven productivity gains lead to a collapse in white-collar employment, labor share falls sharply, demand weakens, asset prices sell off, and policymakers prove unable or unwilling to respond in time. The result is a deflationary spiral with soaring unemployment.

It’s gotten pushback from economists and Fed watchers, especially those who question whether policymakers would really sit on their hands in the face of a disinflationary spiral. You can read a lot about it online. I’m going to use this moment instead as an opportunity to start digging into the macroeconomics of AI in a more disciplined way. This is material I’m learning in public here, please feel free to leave critical and technical comments.

My hypothesis is that AI lowering wages will make it harder for the Federal Reserve to stabilize the economy, and will create an ugly situation in terms of labor share and consumption (both central in Citrini’s story). When I embedded that argument in a leading DSGE framework, one of those predictions held up and the other didn’t.

The simplest, representative-agent New Keynesian (RANK) model doesn’t get us very far. We need income distribution to matter for Citrini’s story, where workers have high marginal propensities to consume (MPCs), capital owners have lower MPCs, and shifting income from one to the other affects demand. At the same time, I don’t want us to get lost in the pyrotechnics of a full heterogeneous-agent New Keynesian (HANK) model, where a continuum of agents generates their own wealth distributions.

A two-agent New Keynesian (TANK) model splits the difference. The model I’m going to use is from “Workers, capitalists, and the government: fiscal policy and income (re)distribution” (2021) by Cristiano Cantore and Lukas B. Freund. They are kind enough to include their Dynare .mod files, which makes replication and modification straightforward, a huge plus. Cantore and Freund describe their model as “tractable laborator[y] for understanding various macroeconomic experiments,” which is exactly what we need.

In this model there are two agents, a worker who works to earn labor market income and a capitalist who doesn’t work and receives profits. (I’m already sold.) Both are forward-looking rational agents. Workers can save in bonds but face portfolio adjustment costs. That friction makes them partially constrained and more responsive to current income than a permanent-income consumer, so they have a higher MPC. The rich capitalist class smooths their entire life’s income independently based on their permanent income.1

In order to explore this, I take their medium-scale model and do my best to insert a task-model loosely based on Acemoglu-Restrepo (2019) (especially read through these Jon Steinsson notes). We take a permanent innovation shock to the automation of tasks with three scenarios: one where the shock is fully labor-augmenting, benefitting workers, a second where it is fully labor replacing, and one in-between.

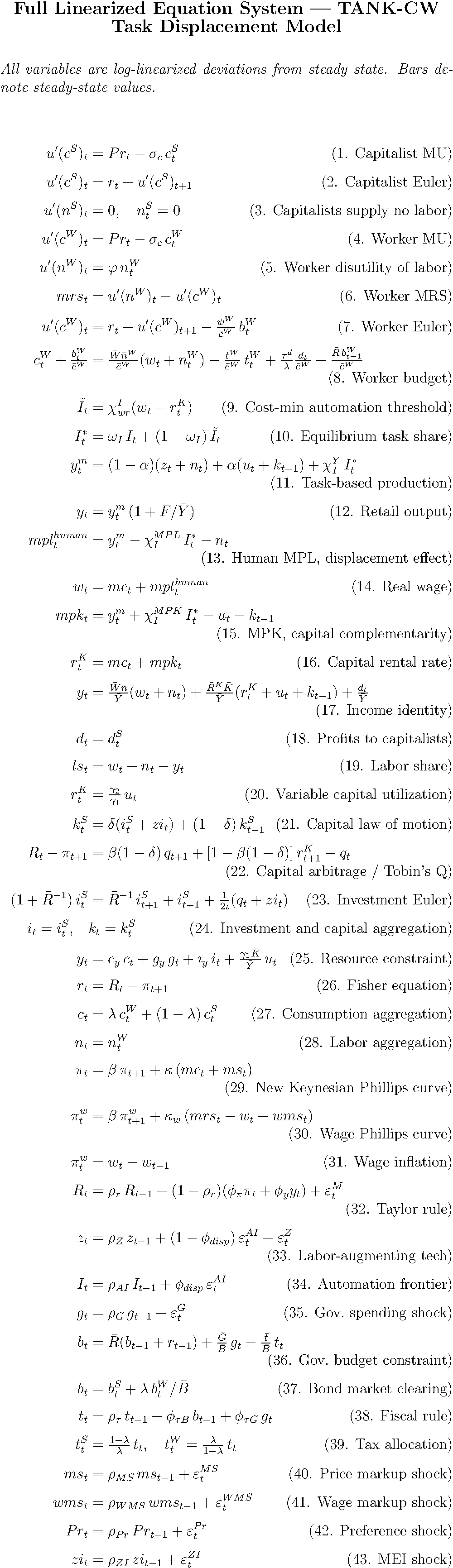

We end up with 43 endogenous equations that we send into MATLAB to be solved.2 (It’s ironic to model the collapse of software while relying on proprietary MATLAB.)

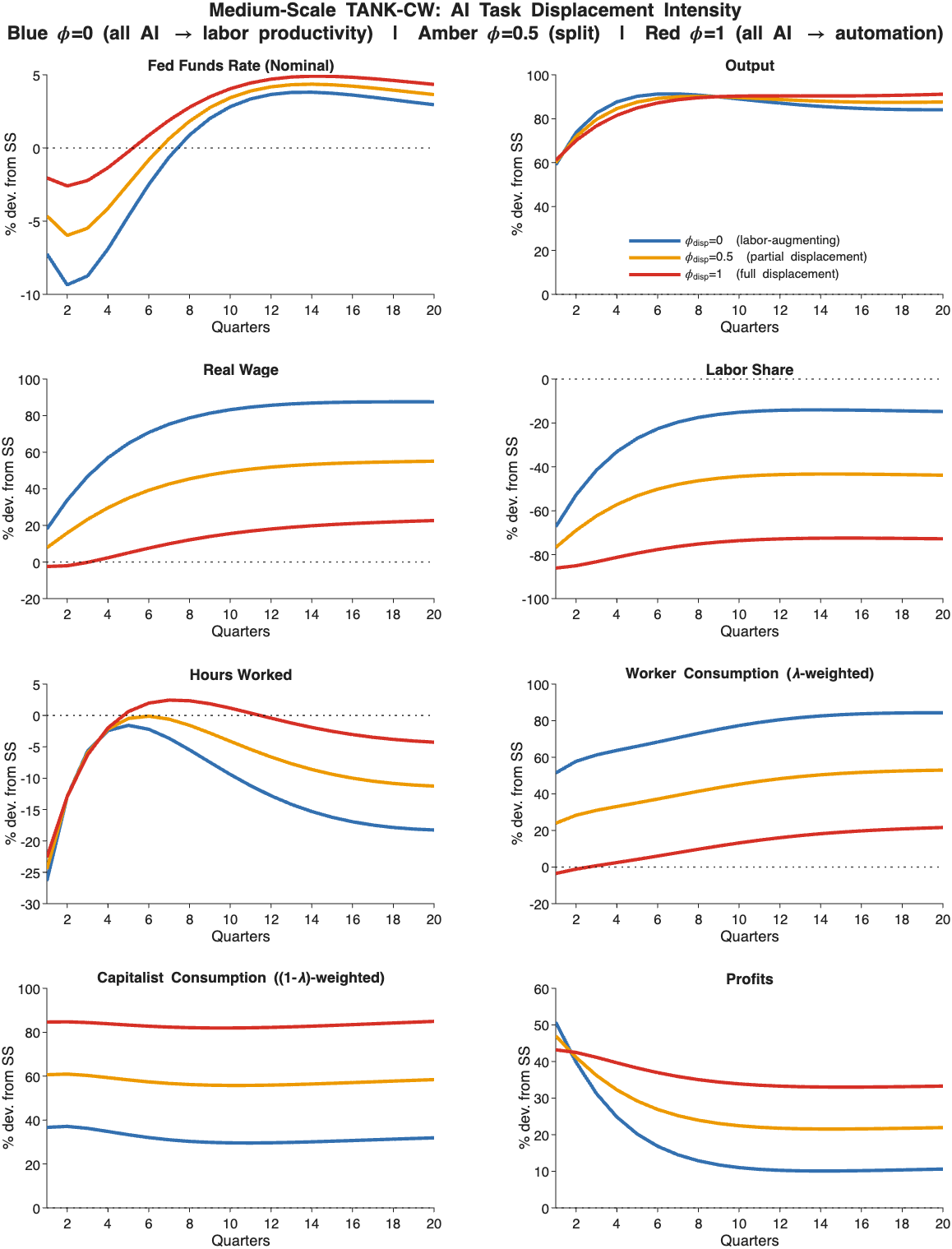

Here’s what we get:

In everyday language, red is where workers get screwed and blue is where workers fully benefit from AI. 0 is the steady-state, or what things were settled at prior to the shock. Don’t worry too much about units, we’re here to see the signs.

What do we see?

Interest rates: All three lines dip below zero, meaning the Fed cuts rates after the AI shock in each scenario. But the cut is dramatically larger under the blue scenario than the red one. This seems backwards. Shouldn’t we expect the scenario where the labor share falls to require deeper cuts?

What I think is happening is mechanical but unintuitive. In the labor-augmenting case, productivity rises faster than wages because of nominal rigidities. Unit labor costs fall sharply, generating deflationary pressure. The Taylor rule responds with aggressive cuts. In the displacement case, human marginal product falls along with wages. Deviations in marginal cost, which is what drives inflation in New Keynesian models, barely moves. So despite the collapse in labor share, there is little disinflation and therefore little pressure for rate cuts.

These kind of New Keynesian results, where inflation is largely about deviations of marginal costs, might feel like its own kind of science fiction. But it’s worth considering. It’s also funny to imagine the Federal Reserve staff who will have to explain to potential new bosses that AI doesn’t magically mean you get to do whatever you want to interest rates.

Workers: It’s not great. In the scenario where workers are augmented by AI they get more consumption and work fewer hours and the labor share fall isn’t that bad. In the displacement case, real wages barely rise, hours initially increase and then drift down, and labor share collapses. The modest rise in worker consumption comes primarily from higher labor supply rather than higher wages. They even, for some periods of the shock, work more hours than the baseline. Their labor share plummets, and their increased consumption is mostly from just working more hours.

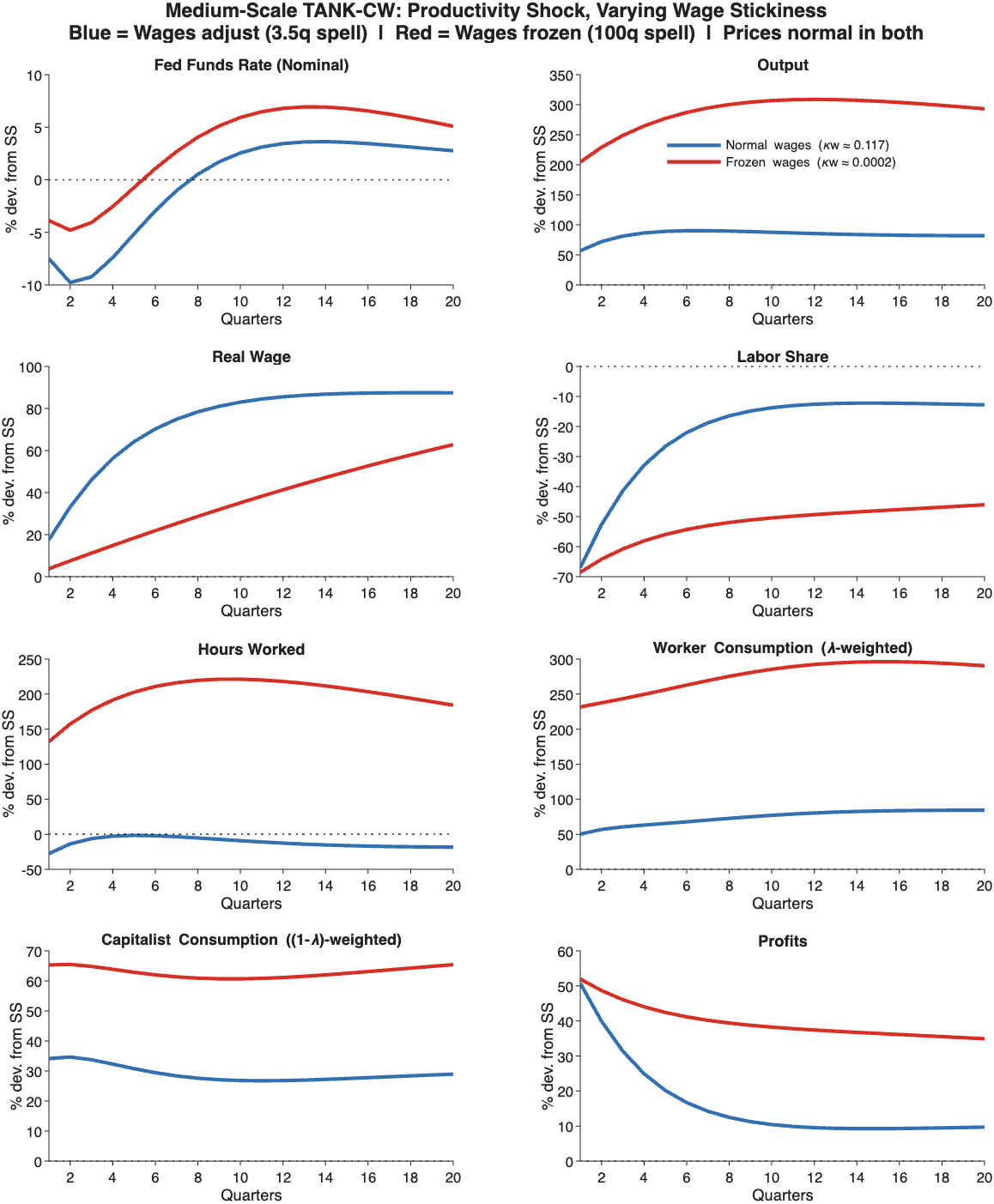

I am still not sure if I’m doing justice to the AI shocks. I get a similar result when I instead just use a productivity shock to the model and make it so wages are fully inflexible, they are basically impossible to update. This extreme example gives us the same kinds of movements.3

From a standard business-cycle perspective, this remains within the reach of conventional macro stabilization. In the displacement scenario, inflation barely moves because marginal cost barely moves, so the Taylor rule doesn’t face dramatic tradeoffs.

That said, I’m still uneasy. If AI were sufficiently disinflationary, or if nominal rigidities behaved differently than in this calibration, we could find ourselves closer to the zero lower bound and facing a more prolonged demand shortfall than this baseline suggests.

I don’t like AI art. But one thing I always do to test the picture and video models is prompt it with “the world as if John Maynard Keynes’s ‘Economic Possibilities for Our Grandchildren’ came true.” In the two videos above you can see Sora, OpenAI’s video producer, from its public launch in October 2025 (top) to a video yesterday (second), each with that prompt, and chart the progress.

So I feel a visceral pain seeing a DSGE model that gives us periods where workers are compelled to work more hours as a result of AI-based skyrocketing productivity. My worry now is less that AI causes a recession. It’s that AI can raise output while worsening workers’ position, a distributional transformation without a traditional macro crisis.

That distributional question of who captures the AI dividend and how it feeds back into demand and political economy is where the real work lies. I’ll be digging into that more in the months ahead.

It’s not worth digging into for the main text, but the worker-capitalist two-agent structure solves a lot of problems that RANK models had, where it’s assumed workers received profits and caused all kinds of bizarre cross-effects like capital profit income driving labor supply. See (Broer et al 2020).

Code here. For the sickos, here’s the whole thing. 9-11, 13, 15, 33-34 are the lines where our additional task-based elements show up:

Funny enough here the Fed cuts less because output is so high because workers are working a lot more hours with their wages frozen. But as a quick check with a completely different methodology it gives us similar results.

Of course AI as being pushed will be a huge push to the upward transfer of wealth and depressive pressure on wages for workers all the way up to workers.

And about the only time in god knows how long that workers hours got reduced was as a reaction to the ACA’s employer mandate to cover people working at least 40 hours a week. Those jobs shrank into 30 hour a week jobs pretty quickly.

Sometimes, the need to scientifically quantify brings darkness instead of light…

The position of workers in our economy has always been precarious throughout history as it has required a neck straining look up to where the decisions that matter are made, rarely for a workers benefit.

Your deep dive toward the truth here is troubling and baffling. I'm skeptical that AI's impact on productivity (total factor?) can't be mitigated with traditional methods via the Fed., a more robust effort toward unionization, minimum wage requirements, fiscal investments to promote jobs and training and so on.

Any way, I'll be intrigued as you continue this reveal into AI potentials, good and bad, as it seems to be a true muddler at present.